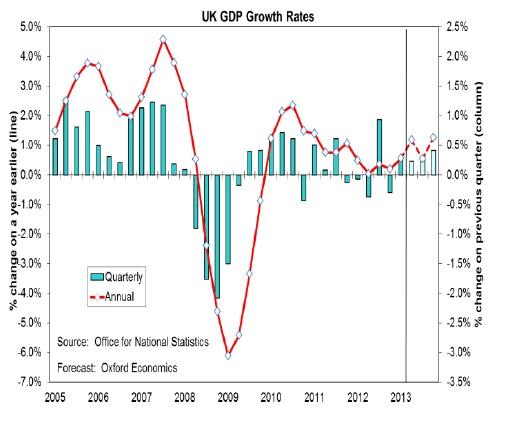

European GDP, 1st Quarter 2023: Data released this week by Eurostat provided a significant update on the European economy, especially for the Euro-zone. The estimate of the trend for GDP in the 1st quarter has been revised to +0.1% for the EU (down from +0.2% in the previous release) and, importantly, to -0.1% for the Euro-zone (from +0.1%).

This now means that the Euro-zone economy meets the definition of a recession with two consecutive quarters of negative growth as the 4th quarter of 2022 was also at -0.1%. However, the EU as a whole is spared this thanks to the marginal increase at the start of 2023 as it had also seen a contraction in the final period of 2022 (-0.2%).

This change has come about because of downward revisions of GDP by a handful of countries, most notably Germany where the trend is now put at -0.3% compared to the previous estimate of “no change”. This also means that the German economy is in a recession, having seen a contraction of -0.5% in Q4-22. Within the Euro-zone, there have also been downward revisions for GDP in Austria (-0.3% from +0.1%) and Ireland (-4.6% from -2.7%), with both also in recession.

This is not a universal trend, however, as some countries have seen marginal improvements in the GDP figures for Q1-23, but as the most significant is Finland (a small economy) which is now put at +1.1% compared to the previous estimate of +0.2%, this is not enough to prevent the Euro-zone figure recording its second consecutive negative movement.

While on the subject of recessions, in addition to the three countries already mentioned, the latest figures show that Estonia, Hungary and Lithuania have also had at least two consecutive quarters with a negative change in GDP.

You can get the full details from the Eurostat News Release which can be downloaded from their website at https://ec.europa.eu/eurostat/news/euro-indicators (8 June) or requested from MTA.

—————————————-

UK Trade in goods, including machine tools, 1st Quarter 2023: Analysis by the Office for National Statistics (ONS) showed a significant narrowing of the deficit for trade in goods thanks mainly to a fall in the value of imports, although there was also a smaller reduction in exports of goods.

Total imports fell by -7.5% (£12.0 billion) compared to the 4th quarter of 2022 while exports fell by -3.2% (£3.4 billion). The change in imports included a fall of £3,5bn in arrivals from the EU, with chemicals (mainly medicinal and pharmaceutical products) down by £1.7bn and a reduction of £1.0bn for machinery & transport equipment. Imports from non-EU countries fell by £8.6bn, driven by a reduction of £2.8bn for machinery & transport equipment (mainly in this case because of reduced imports of electrical machinery from China) and a fall of £2.7bn in fuel imports (mainly gas from Norway).

The smaller decline in exports was more evenly balanced with deliveries to the EU falling by £2.1bn thanks to reductions in the export of fuels (mainly refined products) and chemicals (like imports, mainly due to reduced shipments of pharmaceutical products). Exports to non-EU countries fell by a more modest £1.1bn – this was made up of falls in deliveries of fuels and materials manufactures, off-set slightly by increases in the chemicals and machinery & transport equipment category.

Looking specifically at the trade for machine tools – the only category we specifically monitor on a quarterly basis – UK machine tool exports were worth £131.2 million in the latest period; this is a reduction of -27% compared to the previous quarter (Q4-22) but is only -1% lower than in the equivalent period at the start of last year. Continuing with the comparison against Q1-22, exports to the EU (53% of the total) fell by -2% while shipments to the rest of the world grew by +1%.

Imports of machine tools in the 1st quarter of 2023 were worth £203.7 million; this is virtually unchanged from the previous quarter and, as with exports, only -1% lower than in the 1st period of 2022. We see a different geographical trend for imports with shipments to the EU (58% of the total – the highest ratio since 2013) increasing by +11%, while deliveries to the rest of the world fell by -14%.

There are a couple of issues around data collection that affect both the overall data and the product specific trends. For this comparison, the most important is the Staged Customs Controls which, from the start of 2021, allowed customs declarations to be reported up to 175 days after the date of the import, with full controls reintroduced in July 2022. Therefore, for the first half of 2022 (including he first quarter which is only of the base periods in our comparisons), there is the possibility that arrivals that took place during second half of 2021 are included in the data. Until this fully unwinds, we won’t be able to assess if the trends in the machine tool import figures have been affected.

You can download the ONS Statistical Bulletin with the information on the high-level trade, including by product category from their website at https://www.ons.gov.uk/releasecalendar (12 May) or request if from MTA.