European Industrial Production, January 2024: Eurostat has also published its data although they use Industrial Production (IP) as the top-level aggregate; while the largest part of this is the manufacturing sector, it also includes energy and utilities (but not construction) and the breakdown of the total by sector misses out having a figure for manufacturing.

Total IP for the EU in January was -2.1% lower than in December, with a reduction of -3.2% for the Euro-zone. However, this is distorted by very large swings (up in December and down again in January) for Ireland and, unfortunately, it is not possible to extract them from the overall calculation to get a better idea of the real trends. However, the downturn in January was more than the positive in December and the overall index was at its lowest since September 2021 for the EU and September 2020 for the Euro-zone; this points to weakness in other Euro-zone countries apart from the distortions from the Irish figures.

We can calculate the 3-month rolling trends from the monthly indices published by Eurostat – at the moment this has the advantage of smoothing out the distortions in December and January. In the latest 3 months (November & December 2023 and January 2024) total IP was unchanged compared to the previous period (August, September and October 2023) for the EU and fell by -0.1% in the Euro-zone.

Within the total, the sub-set of the capital goods industries saw a month-on-month fall in output of -12.8% for the EU and -14.5% in the Euro-zone. Compared to January 2023, output of this group declined by -10.1% in the EU and -12.1% in the Euro-zone; for all of these comparisons, this was the weakest of the sub-divisions of IP suggesting that the Irish data is giving the most distortions to the category of most interest to us.

Staying with the 12-month trends, of the 25 Member States for whom the trends are shown (the figures for Czechia and Italy are marked as confidential), total IP increased in 7, was unchanged in one (Spain) and declined in 17. The largest reductions in total IP compared to January 2023 were in Ireland (-34.1%), Estonia (-8.6%) and Bulgaria (-7.6%) while the largest increases were in Slovenia (+12.2%), Greece (+10.5%) and Denmark (+5.3%).

You can get the full details from the Eurostat News Release which can be downloaded from their website at https://ec.europa.eu/eurostat/news/euro-indicators (13 March) or requested from MTA.

—————————————-

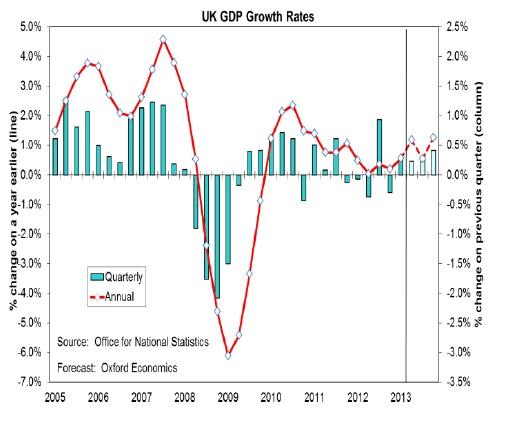

European GDP, 4th Quarter 2023: In its latest update on the GDP data for the 4th quarter of 2023, Eurostat has edged down its estimate for the EU to “no change” (+0.1% in the previous release) but there is no change for the Euro-zone which was also flat compared to the 3rd period of the year.

The GDP growth rate for 2023 has also been downgraded slightly to +0.4% for both the EU and the Euro-zone (it was +0.5% for both groups in the previous estimate).

Although the Euro-zone continues to avoid being in a recession by virtue of having zero growth in the final period of last year, this is not true for some of the individual countries. Estonia and Ireland (although the latter’s GDP data is heavily distorted by HQ operations and this also affects the overall EU and Euro-zone averages) have both had negative GDP growth throughout 2023 and Finland and Sweden were also in recession with negative growth in the final two quarters of the year. In contrast, Austria and the Netherlands which were in a recession saw this ended with growth in the 4th quarter.

You can get the full details from the Eurostat website at https://ec.europa.eu/eurostat/news/euro-indicators (08 March) or requested from MTA.

—————————————-

USMTO and CTMR, January 2024: The US Manufacturing Technology Orders (USMTO) programme tracks orders in the US market, based on the reports from participants. The new year started with orders down by -3.7% compared to January 2023 – it was nearly one third down on the December 2023 figure but that was a very good month, so not really a valid comparison. Of more interest is the fact that although the value of orders was the lowest for January since 2021, the unit count was the lowest since 2016, so demand continues to be driven by specialized and automated machinery.

The AMT Press Release on these results notes that orders from job shops are well below normal levels; as well as their exposure to higher interest rates, it is also noticeable that OEMs in a number of industries are increasing their orders of manufacturing technology equipment. Following a decline of -11% in 2023, the latest forecast is that orders in the US market will grow by +8% this year, although this will not quite reverse the 2023 reduction.

The regional breakdown shows orders for metal cutting machines tools grew in the South-East (+47%), North-Central-East (+22%) and West (+12%) but fell in the North-Central-West (-21%), North-East (-27%) and South-Central (-33%) regions.

The US Cutting Tool Market Report (CTMR) tracks the tooling business on a similar basis and for this part of the market, business was +9.1% higher than in December (which was probably affected by the short working month) and by +4.1% compared to January 2023. As with the machinery market, job shops seem to be the weakest in terms of demand with large OEMs, especially in automotive and aerospace, increasing their purchases of cutting tools.

You can download the press releases for the two surveys from the AMT web-site at www.amtonline.org/topic/intelligence, with the CTMR release also published on the USCTI web-site at www.uscti.com; alternatively, you can request either or both releases from MTA and we can make sure you get them when they are published each month.