USMTO and CTMR, March 2023: The US Manufacturing Technology Orders (USMTO) programme tracks orders in the US market, based on the reports from participants. In the 1st quarter of 2023, orders were -7.5% lower than in the same months of last year (January to March 2022). This was despite a strong increase for March which was one of the largest totals since 2009 and the first at over $½ billion since IMTS last Autumn.

The AMT press release points out that most of the customer sectors saw orders improve with some benefitting from the infrastructure and chips bills that were passed last year and are now being implemented. Construction machinery manufacturers led the way but contract machine shops nearly doubled the February orders figure and both the aerospace and motor vehicle transmissions companies had a significant increase.

Despite this strength, the general economic indicators suggest that a slowdown is on its way with anecdotal comments that quotation activity is slowing.

We continue to see a divergence of trends between the regions; using the metal cutting data (which accounts for 98.5% of the total) as we don’t have all the breakdown for metal forming, the regions continue to be in three groups. The North-Central-East area (+21%) is the only one which is growing, the North-East (+5%), North-Central-West (+2%) and South-Central (-1%) are in a broadly neutral position, while orders have fallen sharply in the South-East (-35%) and the West (-39%).

The US Cutting Tool Market Report (CTMR) tracks orders for tooling on a similar basis. This part of the manufacturing technology spectrum also had an excellent month in March and the total for the 1st quarter is +18% higher than in the same period in 2022. This part of the market continues to improve (the machinery side has been falling while still at a high level) and has yet to get back to its pre-pandemic position, although the 12-month rolling total in March was almost back to the April 2020 level.

You can download the press releases for the two surveys from the AMT web-site at https://www.amtonline.org/topic/intelligence, with the CTMR release also published on the USCTI web-site at www.uscti.com (go to the News Releases tab); alternatively, you can request either or both releases from MTA and we can make sure you get them when they are published each month. We have attached a set of charts tracking the rolling 12-month totals from these two surveys which you can download below.

Japanese Metal Cutting Machine Tools Orders, 1st Quarter 2023: Our colleagues at the Japan Machine Tool Builders Association (JMTBA) also publish monthly orders data although, in this case, it is for manufacturers rather than the market and they only cover metal cutting machine tools (there is a separate association in Japan for manufacturers of metal forming machines).

Orders improved slightly in March with the end of the financial year but the total for the first quarter was -12% lower than in the same period in 2022. This trend was seen in both the domestic (-14%) and export (-11%) markets – orders for metal cutting machine tools are split roughly one-third home and two-thirds export. The 12-month rolling trend

The JMTBA report gives a breakdown of the domestic orders by industry and the two largest in terms of the value of orders are industrial machinery and motor vehicles (which includes automotive parts); compared to the previous quarter (Q4-22), orders changed by +8% and -14% respectively. On this shorter-term comparison, there is an even split between industries where orders have increased and those where they have declined.

However, looking back to the start of 2022, only aerospace (+82%) has seen an increase in orders in the 1st quarter of 2023. In Japan this is a relatively small industry and only accounted for less than 2% of total domestic orders in the latest period.

The largest falls in orders when comparing the 1st quarter of 2023 with the same months of 2022 came in “government, public agencies & schools” (-53%) – this is also the smallest category in both periods – and “trading companies” (-44%) (the next smallest category).

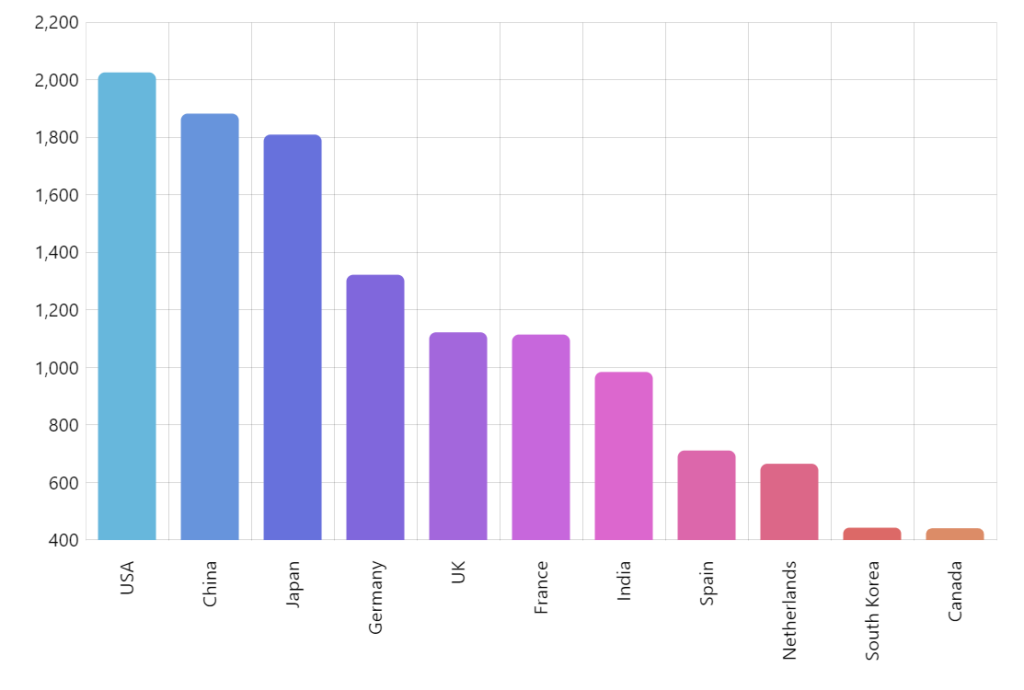

Turning to overseas demand, with total orders down by -11% compared to the 1st period in 2022, export orders from Asia fell by -16%, Europe by just -1% and North America by -13%. The shares of total export orders in Q1-23 accounted for by these regions were 45%, 23% and 29% respectively.

You can access the JMTBA report at https://www.jmtba.or.jp/english/category/machine-tool-orders/ (April 27, 2023) or we can send you the summary of the data – contact Geoff Noon at MTA (email: [email protected]) if you want this analysis. A chart showing the 12-month rolling totals is available to download below.