UK Interest Rate Decision and the Bank of England’s Monetary Policy Report: At its meeting this week, the Bank of England’s Monetary Policy Committee (MPC) voted 6-3 to hold the Bank Rate at 5.25% – after 14 consecutive increases, this is the 2nd meeting at which the MPC has voted to hold rates (the September decision was 5-4).

In his comments at the Bank’s press conference, Andrew Bailey, the Governor of the Bank of England, made it clear that there had been no discussion of reducing interest rates – indeed, although they have probably peaked, he did not rule out needing a further increase. He said that they would “keep interest rates high enough for long enough to get inflation back to the 2% target”. It is worth noting that they expect consumer price inflation to fall to +4.8% for October (the September rate is +6.7%) as the latest round of cuts to consumer energy prices take effect.

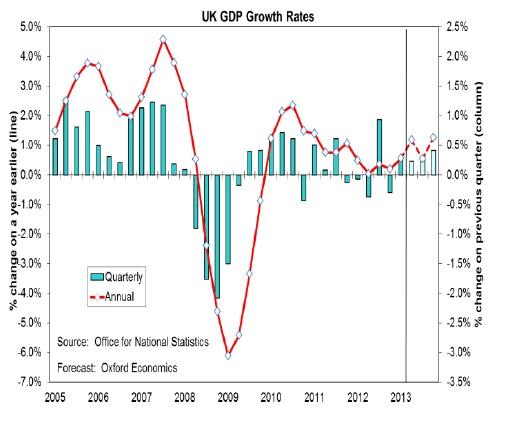

Their projections for activity and inflation are based on an assumption that interest rates stay at the current rate until Q3-2024 before falling gradually to reach 4.25% by the end of 2026. They forecast that GDP will have been flat in the 3rd period of 2023 with nothing more than a marginal increase for the 4th quarter. For next year, the bank has revised its forecasts down and essentially expects no growth, although it is now clear whether or not a recession – two quarters of negative growth – will be triggered.

Their concern over inflation comes from the service sector where rising wages are still driving inflation at a substantial rate that is close to +7% in August. As well as the sharp fall in inflation in October (see above), they expect the rate to be 4.75% in Q4-23, 4.5% in Q1-24 and 3.75% in Q2-24 – it is worth noting that the upper end of the target range for policy decisions is +3% (+2%,±1pp).

The Monetary Policy Report which accompanies the minutes of the MPC meeting this time includes the latest update from the Bank’s local Agents. For manufacturing, they note that the sector continues to be weak with goods exports slowing as contacts continue to report weaker demand and the continued impact of Brexit-related trade frictions. Aerospace and pharmaceuticals remain the main exceptions to the gloomy outlook.

Despite this, investment growth is expected to remain positive in 2024, although at a slower pace than in this year. They note that this will be driven by the need to maintain and upgrade information and other technology, the pursuit of efficiencies and investment to improve sustainability. A special survey by the Agents suggests that the main factors supporting investment intentions are digitalisation, efficiency, and sustainability, while the cost of external finance is the largest reported drag.

You can access the Monetary Policy Report on the Bank of England website at https://www.bankofengland.co.uk/monetary-policy-report/2023/november-2023 with the minutes of the MPC meeting available at https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2023/november-2023.

————————————————————

UK Business investment Analysis by Industry: The Office for National Statistics (ONS) has finally published the breakdown of business investment by industry – for us this means we now have the data, up to the 2nd quarter of 2023, for manufacturing as a whole and the sub-set of the engineering & vehicles industries.

The trends for business investment as a whole are unchanged from those published at the end of September – thanks to the arrival of new aircraft, total business investment in the 2nd quarter of 2023 grew by +4.1% compared to the 1st period of the year and by +9.2% over a year earlier. The rolling 4-quarter (annualized) trend shows growth of +8.3%.

However, the value of this data release is that, for the first time in a year, we now have the breakdown to give us figures for spending by the manufacturing industry and, within that, for the sub-sectors including, most importantly for us, the Engineering & Vehicles industry. Because of the lack of data over the past year, this is the first time we have the figures for 2022 as well as going up to the end of the 2nd quarter of 2023.

For Q2-23, total manufacturing investment (seasonally adjusted and at 2019 prices) was +3.5% higher than in Q1 and +2.3% above the level of a year earlier; the 4-quarter rolling total grew by +0.4%. For the sub-set of the Engineering & Vehicles industry, the quarter-on-quarter growth rate was +5.0% and investment was +5.3% higher than a year earlier, with the 4-quarter rolling total up by +3.6%.

Looking back at the data for the calendar year, 2022 saw total manufacturing investment grow by +0.6% compared to 2021; it accounted for 15% of total business investment – note that this is higher proportion than manufacturing’s share of GDP. Capital expenditure by the Engineering & Vehicles industry grew by +2.3% in 2022 and this sub-sector accounted for 45% of total manufacturing – again this is a larger share than it takes in output.

You can download the ONS datasets (there is no bulletin for this release) from their web-site at https://www.ons.gov.uk/releasecalendar (31 October) or request it from MTA; we also have an analysis of the key data which is available to members – please contact Geoff Noon ([email protected]) if you would like more information on this latest data.