UK Industrial Production, July 2022: The latest data from the Office for National Statistics (ONS) showed manufacturing output unchanged from the level in June; however, we prefer to focus on rolling 3-month periods as this smooths out some of the noise in the data and on this basis, output in the latest 3 months (May, June and July 2022) was +0.3% higher than in the previous period (February, March and April 2022) and +1.7% higher than a year earlier (May, June and July 2021). In July 2022, total manufacturing output stood at 98.9% of its pre-pandemic level (February 2020).

Drilling down into the detail, there is some better news for manufacturing technology suppliers with output of the capital goods group of industries (where most of our customers are classified) in the latest 3 months growing by +3.1% compared to the previous period and +3.7% over a year earlier. However, there is still some way to go before a full recovery can be declared as output in July was only 94.0% of its pre-pandemic level.

There was a varying degree of good news at the industry level as well. The strongest growth was in the automotive industry where output in the latest 3 months was up by +9.7% to a level that was +18.4% higher than the same period in 2021. However, despite this strong improvement, the July output figure stood at 85.3% of its pre-pandemic level, so there is still some way to go, but this latest burst of growth is encouraging.

We also continue to see tentative signs of the aerospace industry sparking into life again although the growth figures here are more modest with the latest 3 months being +1.1% higher than the previous period. Despite this, it was still -8.4% lower than a year ago and the July value is only 62.4% of the pre-pandemic level – by far the weakest of our key industries – so the emphasis is definitely on “tentative”.

The machinery industry is one that traditionally benefits from increased export competitiveness in times of a weak Pound so we might expect the output growth of +1.8% for the latest 3 months compared to the previous period to continue and, hopefully over the next few months to overcome the fall of -5.5% compared to the same months in 2021. Output in July was 101.7% of that recorded in February 2020 and, therefore, one of the few industries that is up on the pre-pandemic level.

Finally, the weak spot at the moment is metal products where output in the latest 3 months is -3.1% lower than the previous 3-month period although it should be noted that the denominator in this calculation includes a “mini-boom” that we saw between February and April and the latest figure is still +6.2% higher than a year earlier and July output is 103.8% of the pre-pandemic level, so the short-term negative for output is tempered somewhat by the overall level being strong.

You can download the ONS Statistical Bulletin on the Index of Production from their website at https://www.ons.gov.uk/releasecalendar (12 September) or request it from MTA; we can also share our analysis of the key industries and sub-sectors if that would be of interest.

————————————————————

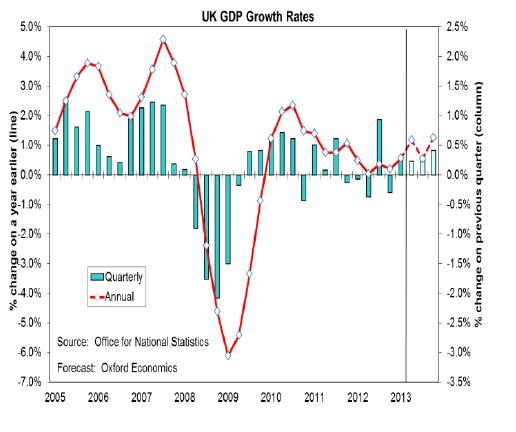

UK GDP, July 2022: As always, the release of the output data for the main sectors of the UK economy, including manufacturing which we report above, also brings the monthly estimate of GDP from the ONS. Following a month-on month fall of -0.6% in June, thanks in part at least to the extra Bank Holiday for the Jubilee, GDP grew by +0.2% in July; this means that over the latest 3 months period, GDP has been unchanged from the previous period.

Although there was a small improvement for manufacturing (see above), the production industries overall saw output fall in July as a result of a sharp reduction in utilities, led by a decline of -4.4% in electricity production, transmission & distribution, probably as a result of higher than usual temperature and some signs of changes in consumer behaviour in the face of higher prices.

Output of the construction sector also fell in July, in this case by -0.8% in July following a reduction of -1.4% in June. The decline in July was entirely due to repair and maintenance activity which more than off-set a slight rise in new work.

The service sector saw output increase by +0.4% in July with consumer-facing services making a slightly higher contribution to that growth than the rest of the sector. The largest contribution to growth in this sector came from information & communication, with computer programming, consultancy & related activities and telecommunications making the largest contribution. Human health & social work activity also grew significantly with increases in GP appointments and critical care offset by a fall in A&E attendances. There was also a small increase in test & trace activity partly off-set by a further reduction in vaccinations.

Among the consumer-facing services, the strongest growth was in wholesale & retail trade with sports activities also growing strongly in a month which included the hosting of both the Women’s Euros and the Commonwealth Games.

You can download the ONS Statistical Bulletin on the monthly GDP figures from their website at https://www.ons.gov.uk/releasecalendar (12 September) or request it from MTA.

————————————————————

European GDP, 2nd Quarter 2022: Eurostat has revised its estimates for European GDP for both the 1st and 2nd quarters of 2022. For the EU, GDP growth is now put at +0.8% for Q1 (revised up from +0.6%) and +0.7% in Q2 (was +0.6%); while these revisions are not that large, they do point to the European economy still being in growth mode in the first half of the year ahead of what will inevitably be a difficult 12-18 months ahead.

The Euro-zone GDP estimates have similarly been revised and now stand at +0.7% in Q1 and +0.8% in Q2 (from +0.5% and +0.6% respectively).

Compared to a year earlier, EU GDP has increased by +4.2% with an increase of +4.1% for the Euro-zone. This is a slower pace of growth than in the 1st quarter (+5.5% in the EU and +5.4% in the Euro-zone) because of the base effect of an acceleration in growth between Q1 and Q2 last year (2021).

Although the growth rates in the first two quarters of the year were similar, the composition of that growth has changed; at the start of 2021 the main driver of growth for the EU was the external trade balance and an increase in inventories but in the 2nd quarter, it is domestic consumption that has lead the way with a contribution from investment and government expenditure.

While there was growth overall, 4 of the EU economies contracted in the 2nd quarter – Poland (-2.1%), Estonia (-1.3%), Latvia (-1.0%) and Lithuania (-0.5%) – with the Portuguese economy unchanged in size compared to the 1st quarter. As none of these contracted in the 1st period of the year (Estonia was flat in Q1), there is not currently a recession in any of the EU countries although the general view is that this will be fairly wide-spread in the second half of the year.

Among the major European economies, Germany only recorded growth of +0.1% in the 2nd quarter so is vulnerable to a revision that could tip it into negative territory. France also had relatively muted growth at +0.5% but both Italy and Spain had relatively goods growth at +1.1% for both economies.

The fastest growing economies in the 2nd quarter were the Netherlands (+2.6%), Romania (+2.1%) and Croatia (+2.0%); this was an acceleration of growth for the first of these but a slower pace than in the 1st quarter for the other two.

For more details, you can download the Euro-indicators report from their website at https://ec.europa.eu/eurostat/news/euro-indicators (07 September).